Innovation portfolio strategy is the planning discipline for new product and new business growth, replacing concentrated, single-bet wagers with a deliberate distribution of resources across a population of opportunities. Innovation portfolio management is the active practice of running that strategy — choosing the mix, scaling investments by evidence, and deciding which projects to continue, pivot, pause, or stop.

New product and new business growth is inherently uncertain. The newer the territory — new to the company's core, or new to the world — the higher the uncertainty, because the assumptions any specific bet rests on are less validated and the operating model required to execute is less established. Sustaining work in established markets behaves differently: the bets are well-understood, outcomes are reasonably predictable, and traditional product-roadmap planning works. New-territory growth doesn't share those properties, and the planning disciplines that work for sustaining work don't transfer.

Portfolio strategy is the planning discipline that does. A growth ambition pursued through a single concentrated bet — one big new product, one major acquisition, one transformational platform play — is a wager the entire growth strategy depends on the bet's particular outcome. Portfolio strategy replaces that wager with something more durable: a deliberate distribution of resources across a population of opportunities, structured so the portfolio as a whole produces the desired growth outcome even though any individual opportunity might fail. The discipline is risk diversification through evidence-based investment scaling.

Innovation portfolio management is the active practice of running that strategy: deciding what mix of opportunities to pursue, how much to invest at each stage, what evidence justifies advancing the next investment, and — most consequentially — which projects to stop. Without portfolio strategy, stage-gating doesn't work; the survival-of-the-strongest dynamic depends on having a pool of candidates so that stopping weak ones frees resources for the strongest. A single project cannot be stage-gated meaningfully. Portfolio strategy is the foundational governance layer that makes all the rest of the innovation discipline possible.

Most enterprise innovation programs run into trouble in one of three places. Some struggle at the level of objectives — there isn't a clear, measurable growth ambition the portfolio is being assembled to achieve. Some struggle with the portfolio strategy and discipline itself — projects are tracked, but the mix isn't intentional, the resource allocations don't match the ambition, and stopping projects is functionally impossible. And some struggle with governance — the corporate operating model that works fine for the core business actively undermines exploration. The problems below cluster into those three layers.

Vague growth ambition. "We want to innovate" or "we need to grow new businesses" is not a portfolio objective. Without measurable success metrics — how much new growth, by when, with what risk tolerance — there's no basis for deciding how big the portfolio needs to be, what kind of projects belong in it, or what counts as success at any stage gate.

Inconsistent logic between investment and target. Many portfolios are funded at a level that mathematically cannot produce the targeted growth, even under optimistic assumptions. The portfolio's investment budget and its growth ambition need to be reconcilable through a credible model — not a hope.

Pipelines confused with portfolios. A pipeline is about process — how ideas move through development. A portfolio strategy is about intentional risk management — how limited resources are distributed across categories of risk and return. Strong pipelines without portfolio strategy produce process without purpose: lots of projects moving through stages, no clear sense of whether the mix is right.

Concentrated bets dressed up as diversified portfolios. Leadership becomes enamored with a bold vision and places massive bets before validating critical assumptions — investing heavily in capabilities for unvalidated markets or platforms whose users haven't been understood. The label says "portfolio." The reality is one or two big bets with some smaller ones along the side.

The project-killing problem. Innovation portfolios only function when projects can be stopped — and many organizations can't stop projects effectively. Sunk costs, executive sponsorship, and the absence of alternatives make termination extraordinarily difficult. Without functional stopping, the portfolio accumulates mediocre projects that absorb resources the strongest opportunities need.

Apples-to-oranges project comparisons. Without a consistent way to evaluate strategies across different projects, decision-makers fall back on subjective advocacy — the project with the best storytelling wins, regardless of evidence. Evidence-based portfolio decisions require evidence captured in a comparable form.

Wrong governance for exploration. Corporate operating models optimized for the core business — predictable, efficient, focused on near-term returns — actively undermine exploratory innovation work, which depends on small bets, fast iteration, and tolerance for failed hypotheses. Running exploration work under optomization focused (exploit) governance is one of the most common portfolio failure modes.

Missing ambidextrous leadership. Portfolio managers without ambidextrous leadership support — leaders who recognize the difference between exploitation and exploration and manage them differently — find themselves blocked at every interface with the core business. RPP misalignment between an emerging venture and the parent organization is, in our experience, the single biggest killer of innovation in large corporations.

Many innovation leaders come from product backgrounds, where the dominant planning artifact is the roadmap: a sequenced commitment to deliver specific products at specific times. Roadmap thinking assumes the bets are known and the work is execution. It rewards precision in forecasting and predictable delivery against committed dates.

Portfolio strategy works differently — and innovation leaders who carry roadmap habits into portfolio work tend to over-commit early, under-stop later, and forecast revenue from opportunities whose viability hasn't been proven. The differences are structural:

Roadmaps are deterministic; portfolios are non-deterministic. A product roadmap commits to specific products being delivered. A portfolio defines target attributes — the kind of opportunities the portfolio intends to pursue — and explores many concepts in pursuit of those targets, knowing most will fail.

Roadmaps emphasize specific opportunities; portfolios emphasize the whole. Performance is judged at the portfolio level, not the individual project level. An individual project that fails after being correctly stopped is a successful contribution to the portfolio — it freed the resource for the next candidate.

Roadmaps commit to revenue forecasts up front; portfolios commit revenue forecasts only at scaling. A common failure mode is treating early-stage opportunities like roadmap items — building revenue expectations from the concept stage and managing the portfolio to those numbers. Revenue forecast commitments shouldn't happen until the scaling stage, when in-market evidence supports them. Earlier than that, what's modeled at the portfolio level is the probability distribution of outcomes across the population of bets.

The mental model shift is the same one that distinguishes venture investors from product managers. Both are useful. They are not the same discipline.

Three levels of strategy operate in an enterprise innovation program, and the Portfolio is Level 2 — sandwiched between the corporate growth strategy that sets the ambition and the individual project strategy hypotheses that pursue specific opportunities:

A portfolio is a defined collection of new product or business projects sharing a common methodology and governance structure. It is a population of bets, not a list of projects. Some of those bets are fully modeled and tracked; others may be tracked only at a high level — initiatives outside the formal innovation system, such as skunkworks, BU-funded experiments, or M&A pipeline candidates — but still accounted for in the portfolio view because they consume resources and contribute to the growth ambition.

A portfolio objective is the outer-loop grounding for everything in the portfolio. Just as each individual project is grounded by its Opportunity Goal — the specific aspiration it pursues — the portfolio is grounded by the Portfolio Objective: a measurable statement of what growth outcomes the portfolio is being assembled to deliver. Without a Portfolio Objective, there's no anchor for evaluating whether the portfolio's mix, size, allocation, or pace is appropriate.

Larger organizations may need portfolio hierarchies — multiple portfolios nested under enterprise-wide views, organized by business unit, geography, strategic theme, or any dimension that matches how innovation is governed. Each sub-portfolio has its own objective and configuration; the enterprise view aggregates them.

Portfolio mix is the intentional distribution of projects across categories that operationalize the portfolio's growth objective. It is the most consequential decision in portfolio strategy and the one most often skipped or made by default. The categories that make up the mix are called Project Classes.

The right project classes depend on what the growth objective actually calls for. Diversification across the core-adjacency spectrum calls for classes like Core / Adjacent / Disruptive. Diversification into recurring-revenue services calls for classes defined around business model — physical-only / hybrid / pure-service. Geographic diversification calls for classes defined by region; technology-domain diversification, by domain. The classes are configurable per portfolio. What's universal is the requirement that the mix be intentional and that the classes correspond to the diversity dimensions the growth objective demands.

Two requirements distinguish a real portfolio mix from a list of projects:

The mix must align with the objective. If the growth ambition calls for diversification away from the core business, the mix needs adjacent and disruptive bets in defined ratios. If the ambition calls for moving into recurring-revenue services, the mix needs explicit allocation to service-bearing project classes. The mix is the strategy translated into a category-level distribution.

Each class needs its own profile. Different project classes have systematically different investment levels, time-to-market, adjacency risk, financial profiles, and survival rates. They cannot share a single set of stage-gate guidelines. A disruptive project burning $5M to test a new business model needs different time and budget guardrails — and different evidence standards — than a core project iterating a new feature. Stage allocations, survival rate assumptions, evaluation criteria weightings, and evidence requirements all need to be calibrated per class.

Allocation should be measured in resources, not just project count. Per-class resource intensity may vary materially — a single Disruptive bet may consume several times the headcount and capital of a Core project at the equivalent stage. A portfolio that targets "30% Disruptive by project count" can land at 70% of total investment in disruptive work, or 5%, depending on which specific projects sit in that class. Mix targets should be set primarily in resource terms — share of investment dollars and headcount — with project count derived from the per-class profile and used as a secondary check on front-of-funnel optionality.

The most widely useful project class taxonomy for mature companies is the core-adjacency one. Two reasons.

First, diversification along the core-adjacency axis is the most common growth objective for mature companies. When the core business slows, growth has to come from somewhere else, and "somewhere else" almost always means outside the current product-market combination. Most enterprise growth ambitions reduce, eventually, to some intentional movement away from the current core.

Second, core proximity is the variable most directly correlated with the hardest-to-mitigate failure mechanism — RPP misalignment. Company-fit risk increases sharply with distance from the core: existing resources, processes, and priorities are tuned to the current business, and a project that violates those assumptions runs into invisible structural resistance. RPP misalignment is, in our experience, the single biggest killer of innovation in large corporations — and it is the failure mode most easily anticipated by the project's adjacency class.

The three classes:

Core Innovation — Enhancements or new versions of existing products, expansion to closely adjacent market segments. Same product domain, same or closely adjacent markets, same business model, same position in the value chain. Lowest risk, highest synergies with the existing business, smaller incremental impact.

Adjacent Innovation — New products within an existing line of business with the same business model, sold into closely adjacent market segments. Or existing products extended into new markets. Moderate risk; moderate synergies; meaningful but bounded growth potential.

Disruptive (Transformational) Innovation — New business models, new market segments, new positions in the value chain. Highest risk and highest RPP misalignment, but also the highest incremental growth and impact potential. This is where future core businesses come from — and where corporate operating models tend to do the most damage.

Growth Forge ships Core / Adjacent / Disruptive as the default project class taxonomy. Portfolios can be configured with custom classes when the growth objective calls for a different diversity dimension.

A portfolio strategy isn't a slogan or a project list. It is a defined configuration with five things specified intentionally.

1. Diversity vectors. The dimensions along which the portfolio diversifies — typically the project class definitions discussed above, plus secondary vectors as needed (time-to-market profile, technology domain, geography). Diversification is the mechanism that turns growth ambition into a collection of bets.

2. Allocation targets across categories. The intended distribution of resources across the classes defined in step 1 — primarily as a share of investment dollars and headcount, with project counts derived from per-class profiles. "40% of innovation investment in Core, 35% in Adjacent, 25% in Disruptive" is a portfolio strategy. "We're working on innovation" is not.

3. Per-stage evidence requirements and investment limits. What evidence advances a project from one stage to the next, and what level of investment is authorized at each stage. Investment scales with confidence; confidence comes from evidence; evidence requirements scale with each stage gate.

4. Termination protocols. Explicit criteria for stopping projects — independent of sponsorship, sunk cost, or political weight. The portfolio only works if termination works.

5. Periodic rebalancing cadence. A regular review — quarterly is typical — that re-examines whether the actual mix matches the target, whether the target still matches the growth ambition, and whether resource allocation should shift in response to new evidence or environmental change. Without rebalancing, portfolios drift toward whatever has the loudest sponsor.

Portfolio strategy operates on top of the Innovation Pipeline — the stage-gated investment structure within which individual projects develop. Each stage gate is a discrete investment decision (Continue, Pivot, Pause, or Stop) made on the strength of progressively higher evidence requirements. The funnel is what those stage gates produce when applied consistently across a population of projects: healthy innovation portfolios start many more concepts than they ever launch, with early stages designed to have low survival rates. This is the survival-of-the-strongest mechanism in operation — stopping weak projects early and cheaply is what frees the resources that let the strongest projects scale. (For how the stage gates themselves work, see BRI's Staged Innovation Methodology.)

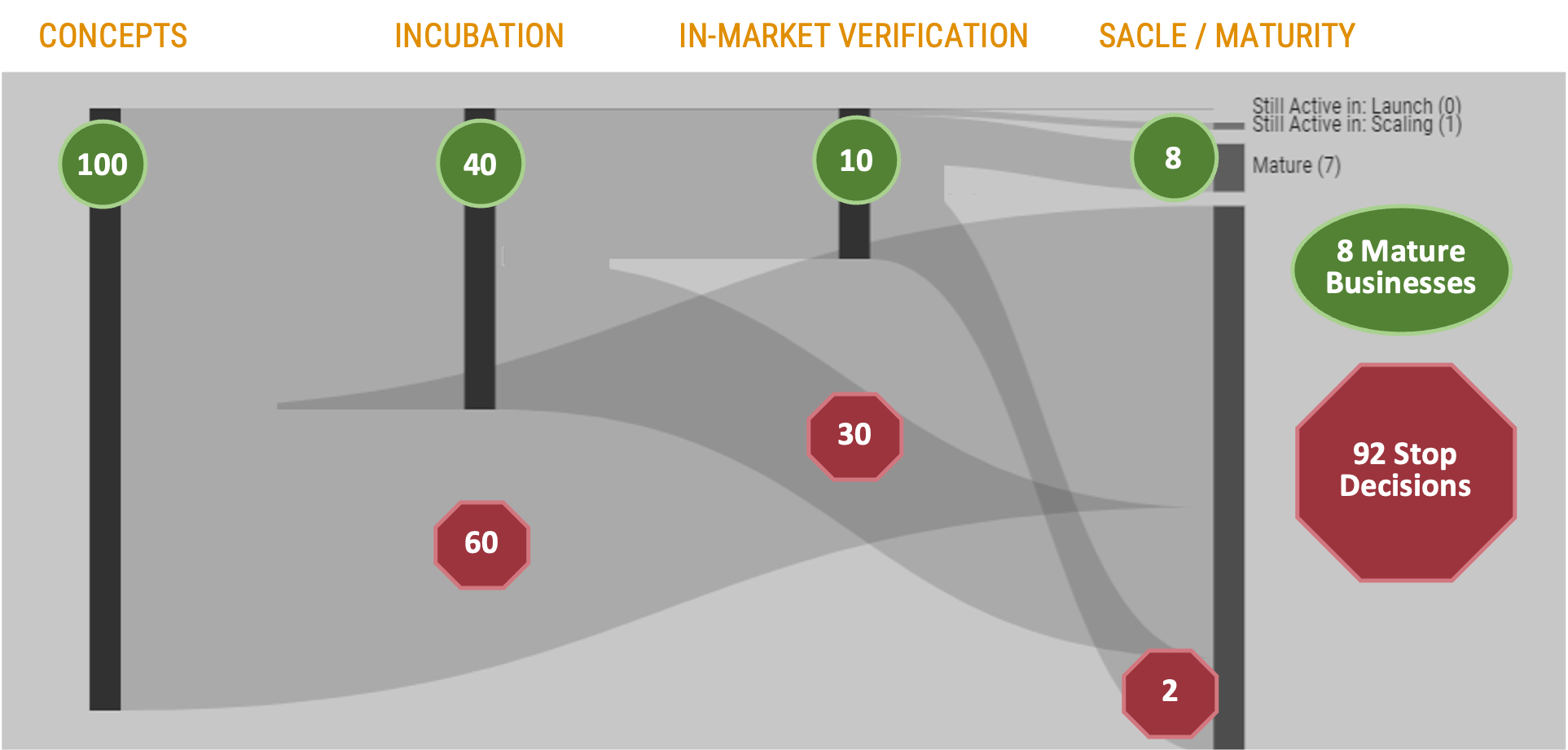

A representative shape for a mature company's innovation portfolio:

Starting 100 concepts to land 8 mature businesses — a 92-stop ratio — looks alarming until you compare it to the alternative: starting 8 concepts and trying to force all 8 to survive. The forced version produces mediocre launches, not eight winners. The funnel produces eight strong launches because it stopped 92 weaker ones.

This dynamic only functions at portfolio scale. A program with two projects cannot meaningfully stop one of them — the portfolio loses 50% of its activity, and the political economics of stopping become impossible. The funnel dynamic is what makes the larger investment in early-stage activity worth it: a healthy front-of-funnel produces the optionality that allows late-stage discipline.

Portfolio outcomes are inherently uncertain — even a well-managed portfolio cannot promise that any specific project will succeed, only that the population of bets will likely produce a particular distribution of outcomes. Portfolio modeling makes this explicit. Using Monte Carlo simulation against archetypal cashflow profiles per project class — typical revenue, investment, time-to-market, and survival ranges — combined with a defined number of project starts per year, the model produces probability distributions for portfolio resource investment, revenue and profit by class, and aggregate fallout by stage.

This kind of model serves two practical purposes. First, it lets a portfolio manager forecast the scale of investment fund required to deliver a given growth ambition. Second, it sets realistic per-stage benchmark ranges against which the actual portfolio can be measured. Profile types with higher failure rates may need to be deliberately over-weighted at the concept stage to deliver the desired mix at later stages — and the model is what reveals that.

The five elements above describe what a portfolio strategy contains. Custom governance describes the operating environment those elements function in — and for any portfolio that includes disruptive innovation, governance design is not an auxiliary topic but a core part of the portfolio discipline itself. Pursuing disruptive growth inside a mature company creates a structural tension that custom governance is the only known solution to.

The value of pursuing disruptive growth inside a mature company — rather than spinning it out — comes from synergies with the core business: brand, customer relationships, channels, technology base, operational infrastructure that an external startup would have to build from scratch. But the more disruptive the innovation, the more its operational requirements diverge from the core — and the more the parent's RPPs (Resources, Processes, Priorities) actively obstruct the work. A disruptive project needs a hiring exception in the middle of a hiring freeze. It needs to ship a "good enough" MVP from a brand built on premium quality. It needs the sales force to sell something that isn't in their compensation plan. Each of these is a structural conflict, not a misunderstanding to be resolved with a meeting. The cumulative effect of too many of them will eventually kill the project either form political frustration or competitive disadvantage.

The catch-22: synergy with the core is the reason to do it inside; misalignment with the core is the reason it can't survive inside. Both pressures are real.

The resolution is custom governance — deliberately differentiated operating models for innovation work, calibrated to the venture's stage and core proximity. Not full independence (which sacrifices synergies) and not core integration (which sacrifices the project), but an intentional balance designed to evolve as the venture matures.

Different combinations of core proximity and venture maturity call for different governance approaches. A close-to-core concept-stage project might be governed within an existing R&D function. A transformational concept might belong in an exploratory R&D group or external CVC arrangement. As ventures mature toward scaling, governance progressively shifts from autonomous toward more integrated — the goal at maturity is to capture the synergies that justified doing it in-house, without prematurely smothering the venture in core-business processes.

A common pattern across stages:

The Mezzanine stage is the most consequential and most often mismanaged. Premature integration of a scaling venture into core governance is one of the most common ways mature companies kill businesses they spent years building. Mezzanine governance is explicitly designed to manage that handoff — phasing in synergies as the venture's operational maturity allows, rather than imposing them all at once.

Custom governance only functions when supported by ambidextrous leadership — leaders who recognize that exploration and exploitation require different mental models, decision speeds, and risk tolerances, and who actively manage both. Ambidextrous leaders carry the authority to negotiate exceptions to core-business defaults on behalf of innovation projects.

A practical organizational mechanism for operationalizing this is a Functional Interface Team (FIT) — a cross-functional group with representatives from each major function (HR, Finance, Legal, IT, Sales, Operations) empowered to grant exceptions, design alternative processes, and resolve RPP conflicts on behalf of innovation work. The FIT team is what prevents every interface friction from escalating to executive review or unduely slowing the venture.

Portfolio managers track a small number of high-leverage measures over time, against the targets set in the portfolio strategy.

Resource allocation by stage and class. Are time, capital, and headcount being deployed against the stages and classes the strategy calls for? Resource allocation is the primary mix measure, and it can drift even when project counts look on-target. Drift between actual resource allocation and target is the most common signal that a portfolio is shifting away from its objective.

Portfolio mix. Does the actual distribution of projects across classes match the target distribution? Mix drift typically appears at the front of the funnel first, as starts skew toward whichever class is easiest to launch, regardless of strategic intent.

Survival rates by stage. Are the actual stop/continue ratios producing the funnel shape the model called for? Survival rates that are too high — projects passing every gate — are usually a sign the gates aren't actually gating, not a sign of a strong portfolio.

Individual project performance vs. stage and class guidelines. Are projects hitting their per-class benchmarks, or running over time and budget? Projects materially outside class guidelines need either a guideline revision or a stage-gate decision.

The discipline is the periodic reconciliation: actual against target, mix against ambition, performance against guidelines. Where the picture has drifted, the portfolio either gets rebalanced or the strategy gets revised. Either is a legitimate response. Drift accumulating without reconciliation is the failure mode.

For organizations large enough to need it, sub-portfolio configurations support the same tracking at division, geography, or strategic-theme level — with rollups to the enterprise view that preserve operational detail while supporting aggregated decisions about resource shifts across sub-portfolios.

A pipeline is about process — how ideas move through stages of development with progressively higher evidence and investment requirements. A portfolio is about intentional risk management — how a defined population of opportunities is assembled, allocated across categories of risk and return, and managed to deliver a specific growth objective. A pipeline without a portfolio is process without strategic purpose: lots of projects moving forward, no clear sense of whether the mix is right or whether the result will achieve the corporate growth ambition.

Stage-gating depends on a portfolio. Without a population of opportunities, the survival-of-the-strongest dynamic — the mechanism that turns progressive evidence into progressive investment — has nothing to operate on. A single project can't be stage-gated meaningfully because there's no alternative to redirect resources to. Portfolio strategy is what makes the pipeline discipline functional, what makes intentional resource allocation possible, and what gives stage-gate decisions strategic context. It is the layer underneath, not the layer alongside the Innovation Methodology & Staged Pipeline.

Start with the corporate growth objective. The mix has to operationalize that objective — not a generic best-practice template. Diversification along the core-adjacency axis calls for Core / Adjacent / Disruptive in defined ratios. Diversification toward recurring-revenue services calls for classes around business model. Geographic diversification calls for classes by region. Once classes are defined, each needs its own profile (typical investment level, time-to-market, survival rate, evidence standards) — different classes cannot share one set of stage-gate guidelines. Core / Adjacent / Disruptive is the most widely useful starting taxonomy because adjacency-based diversification is the most common growth objective and core proximity is the variable most directly correlated with RPP misalignment risk.

Resource allocation is the primary measure; project count is a secondary check. Per-class resource profiles vary materially — a single Disruptive bet may consume several times the headcount and capital of a Core project at the equivalent stage, so a "30% Disruptive by project count" target can land at 70% of investment, or 5%, depending on which projects sit in that class. Set mix targets in dollars and headcount; let project counts follow from per-class profiles. A common failure mode is drifting away from resource intent while project counts continue to look fine on the dashboard.

Because that's the mechanism that produces strong outcomes. A healthy portfolio that starts 100 concepts to land 8 mature businesses produces eight strong launches because it stopped 92 weaker ones — freeing the resources, attention, and organizational capacity that the eight winners progressively needed as they matured. The forced alternative — starting 8 concepts and trying to make all 8 succeed — produces few mediocre launches, not eight winners. Early stopping is cheap; late stopping is expensive; never stopping is catastrophic. The funnel dynamic is the design choice that makes the math work.

Three things have to be in place before stopping becomes possible. First, explicit termination criteria defined before the project starts — what conditions trigger a stop, independent of sponsorship. Second, continuous opportunity flow — a backlog of promising alternatives waiting for resources, so stopping isn't experienced as loss but as redirection. Third, a culture that treats stopping as smart resource allocation, not failure — visible reinforcement that good stopping decisions are part of what success looks like, including for the leaders who recommended the stop. None of this is easy, but in our experience, the absence of these three is the most common reason innovation portfolios accumulate mediocre projects.

Project financial forecasting models the expected outcome of a specific opportunity, assuming a defined strategy. Portfolio modeling treats individual outcomes as inherently uncertain and instead models the distribution of outcomes across a population of bets. The Growth Forge Portfolio Modeling Tool runs Monte Carlo simulation across archetypal cashflow profiles per project class and produces probability distributions for portfolio investment, revenue, profit by class, and aggregate survival rates. The output isn't "this portfolio will deliver $X" but "this portfolio has an N% probability of delivering between $X and $Y, given these inputs." That distinction matters because it sets honest expectations and supports real conversations about whether the portfolio's investment level matches its growth ambition.

Quarterly is a typical cadence for active portfolios — frequent enough to catch drift early, infrequent enough not to thrash on noise. The review covers three questions: does the actual mix match the target mix; does the target mix still match the growth ambition; and does resource allocation need to shift in response to new evidence or environmental changes. Rebalancing without reconciliation against the corporate growth objective is just bookkeeping. The objective itself should be reviewed less frequently — typically annually, or when a meaningful environmental shift demands it.

Pursuing disruptive growth inside a mature company creates a structural tension. Doing it in-house is justified by synergies with the core — brand, customers, channels, technology, infrastructure. But the more disruptive the innovation, the more its operational requirements diverge from the core's existing Resources, Processes, and Priorities, and the corporate operating model — optimized for predictable exploitation — actively obstructs the work. Custom governance is the resolution: deliberately differentiated operating models, calibrated to venture stage and core proximity, that capture synergies while protecting the venture from RPP misalignment. Without it, the parent organization tends to either smother the venture or extract it (failed spin-out, failed M&A integration), neither of which delivers the synergistic value that justified doing it in-house in the first place.

Growth Forge operationalizes the portfolio discipline as an integrated platform: configurable methodology per portfolio (custom pipeline stages, investment guidelines, evaluation criteria); real-time portfolio dashboards (project distribution, resource allocation, investment performance, progress tracking); evidence-based project comparison using the BRI Strategy Framework and the DFV evaluation lens; sub-portfolio organization with enterprise rollups; external project tracking; Monte Carlo portfolio modeling across project class archetypes; and streamlined status management to eliminate the spreadsheet-chasing that absorbs most portfolio managers' time.

Framework concepts:

Methodology and strategy:

Related reading:

See it in practice: